Canada sidesteps recession—but key risks remain

You should also check out

Global Economic Outlook for Canadian exporters

What shifting global conditions, rising costs and uneven growth mean for your export decisions in 2026.

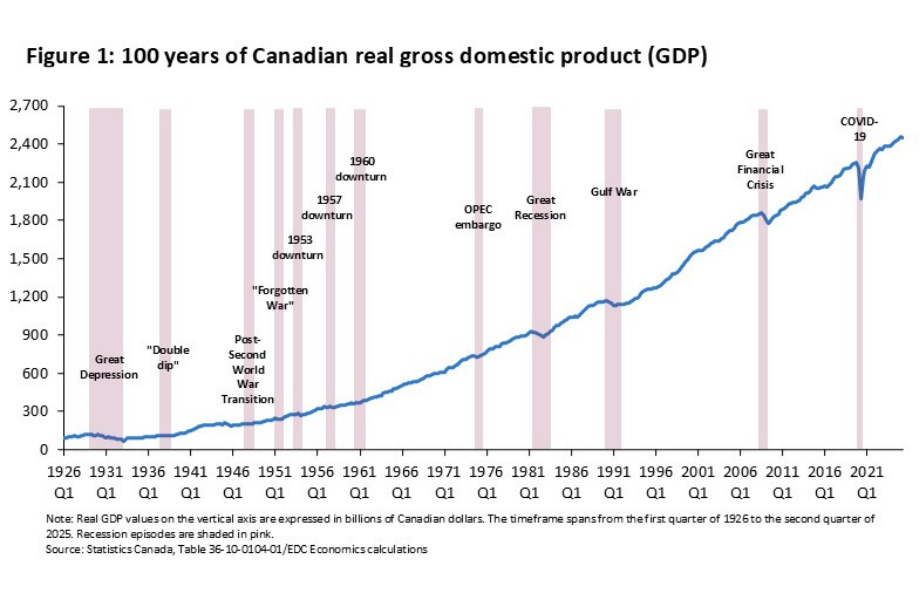

Canada’s recession history highlights ongoing risks for 2026

Downside risk No. 1: Trade disruptions and tariff shocks

You should also check out

-

Top 10 global risks for Canadian exporters in 2026

Discover the Top 10 global risks for Canadian exporters in 2026—from CUSMA talks to trade wars and recession threats. Learn how to prepare with EDC insights.

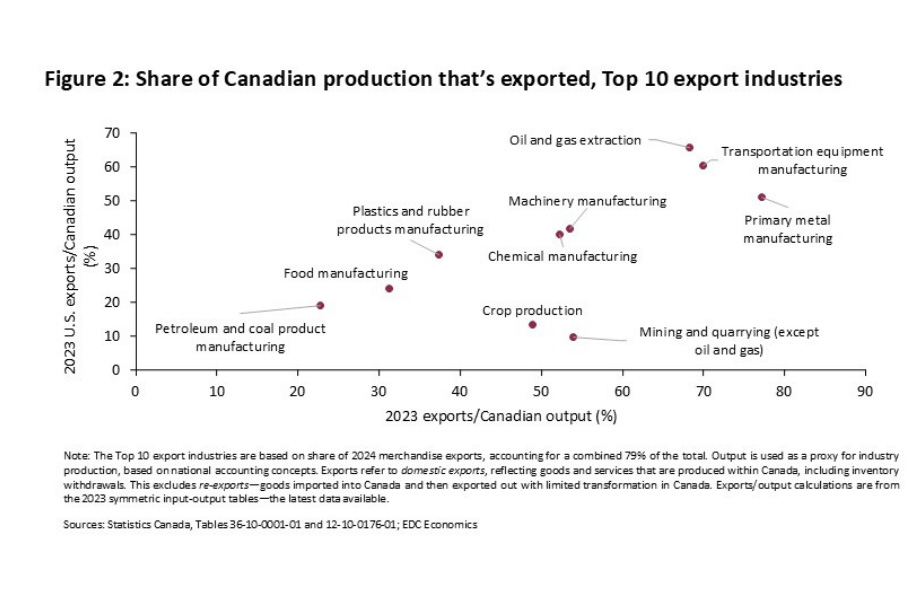

Canada’s export dependence amplifies trade risk

What are the Canadian sectors most exposed to tariff shocks?

Sector spotlight: Autos, steel, aluminum and forestry

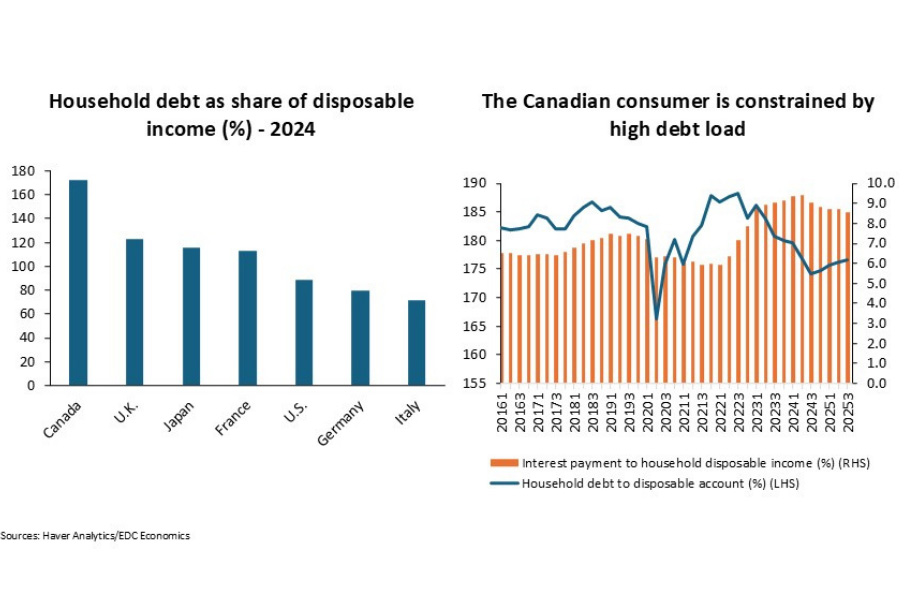

Downside risk No. 2: Weakening consumer demand