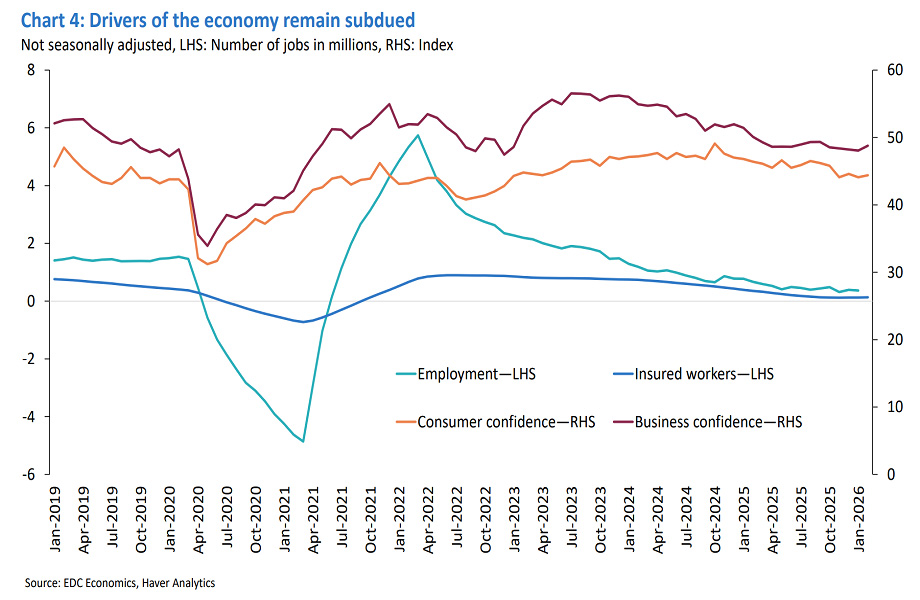

North America’s economies weathered trade headwinds in 2025 better than expected, with growth exceeding forecasts and recession avoided across the region. Even so, momentum slowed late in the year as uncertainty disrupted business and household spending plans.

Economic anxiety remains elevated. Spillover effects from the ongoing conflict in the Middle East have added to uncertainty ahead of this summer’s review of the Canada-United States-Mexico Agreement (CUSMA), clouding the outlook for trade and investment.

One limited support to the outlook emerged in February, when the U.S. Supreme Court overturned the administration’s broad use of emergency tariff powers. However, relief is limited. Officials have signalled a shift toward slower-moving, sector-specific tariffs, leaving trade policy uncertainty firmly in place.

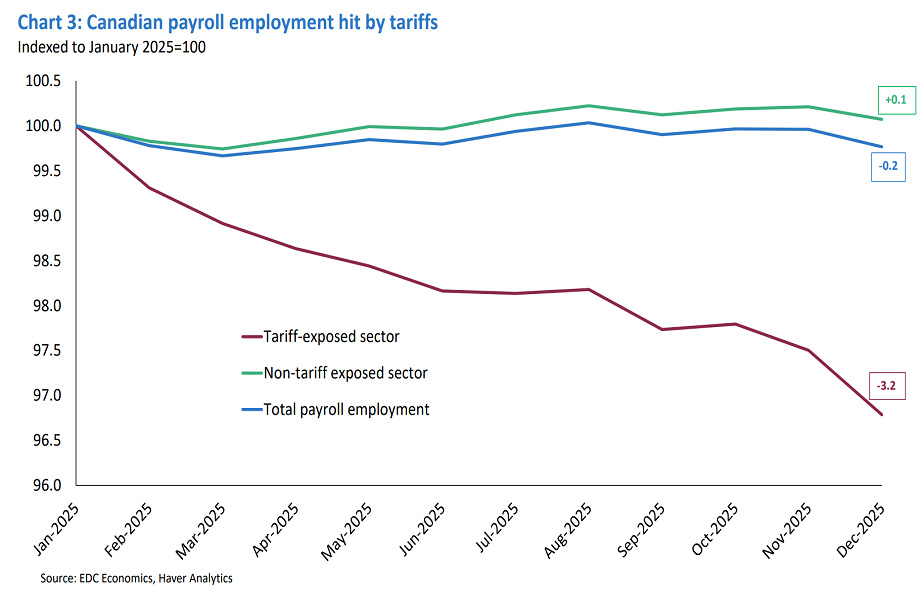

Across the continent, hiring has eased and is likely to remain subdued through the first half of 2026 as businesses delay major investment and hiring decisions until greater policy clarity around CUSMA emerges. Elevated uncertainty continues to weigh on overall economic activity.

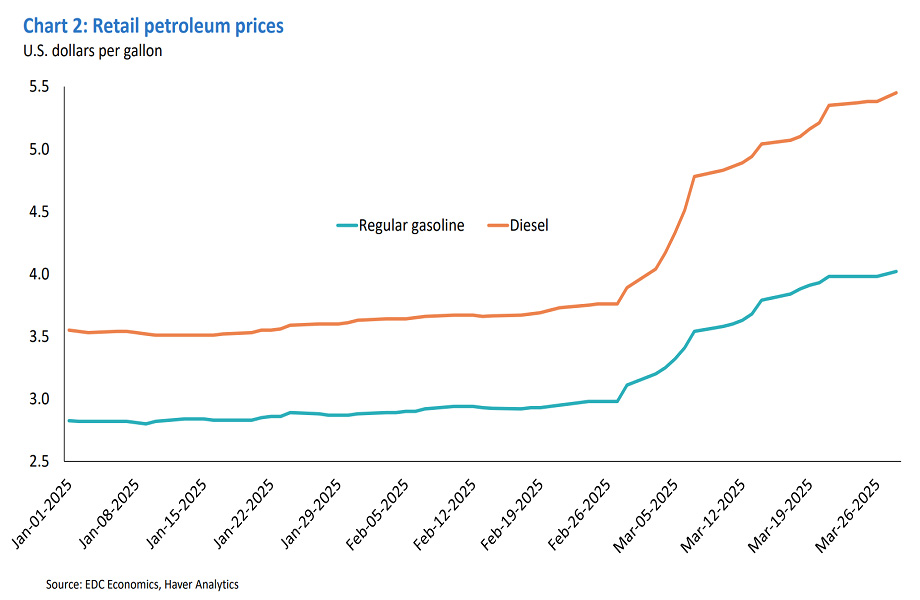

At the same time, conflict-driven pressure on energy and commodity markets is expected to push inflation higher. Central banks across North America are likely to proceed cautiously, balancing rising price pressures against weakening growth. Higher living costs will further strain lower-income households and dampen consumer demand.

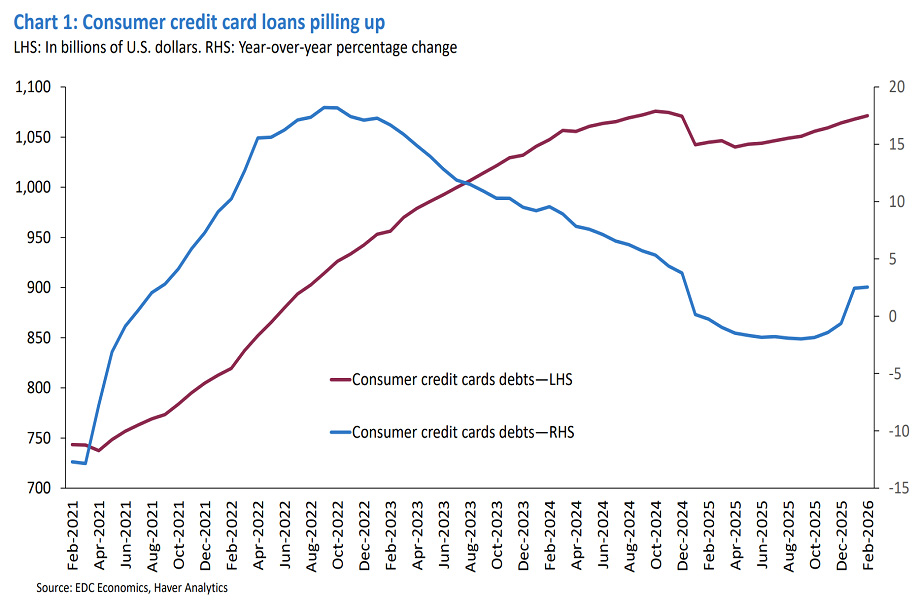

These risks come against a backdrop of high household debt. Elevated mortgage rates and housing supply shortages continue to constrain construction in Canada and the United States, keeping affordability out of reach for many families and limiting discretionary spending across the continent.

For practical guidance on managing export risk amid ongoing trade uncertainty, watch Export Development Canada’s webinar, Navigating trade volatility in 2026, which explores ways to protect cash flow, manage risk and reduce dependence on the U.S.