Canada’s aerospace industry: Global powerhouse enters a new era

You should also check out

Rising energy prices and trade tensions are reshaping the global economic outlook. Explore what it means for growth, trade and Canadian exporters.

From pandemic disruption to aerospace industry recovery

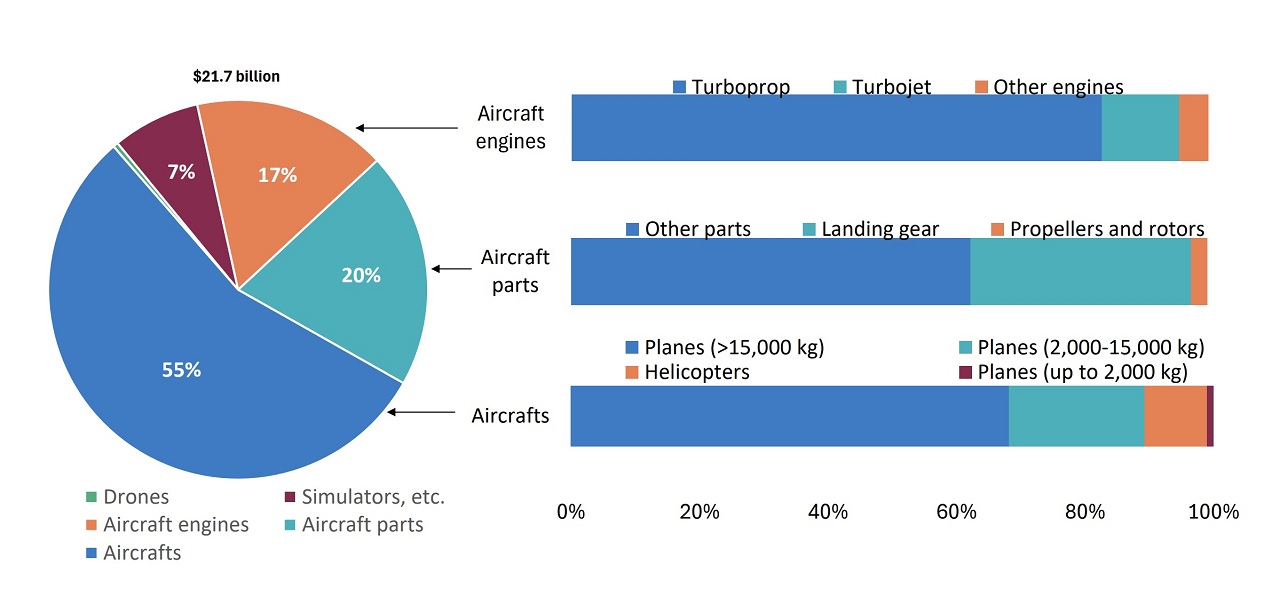

Figure 1: Canadian aerospace exports, 2024 (nominal, customs basis)

Source: Canadian International Merchandise Trade (CIMT) dataset

Note: Values are nominal, customs‑basis. Estimates are below AIAC equivalents, as the CIMT data definition is narrower. Simulator, etc. includes arrestors and launchers.

Aerospace exports and Canada’s key industry strengths

Key aerospace export markets and trade risks

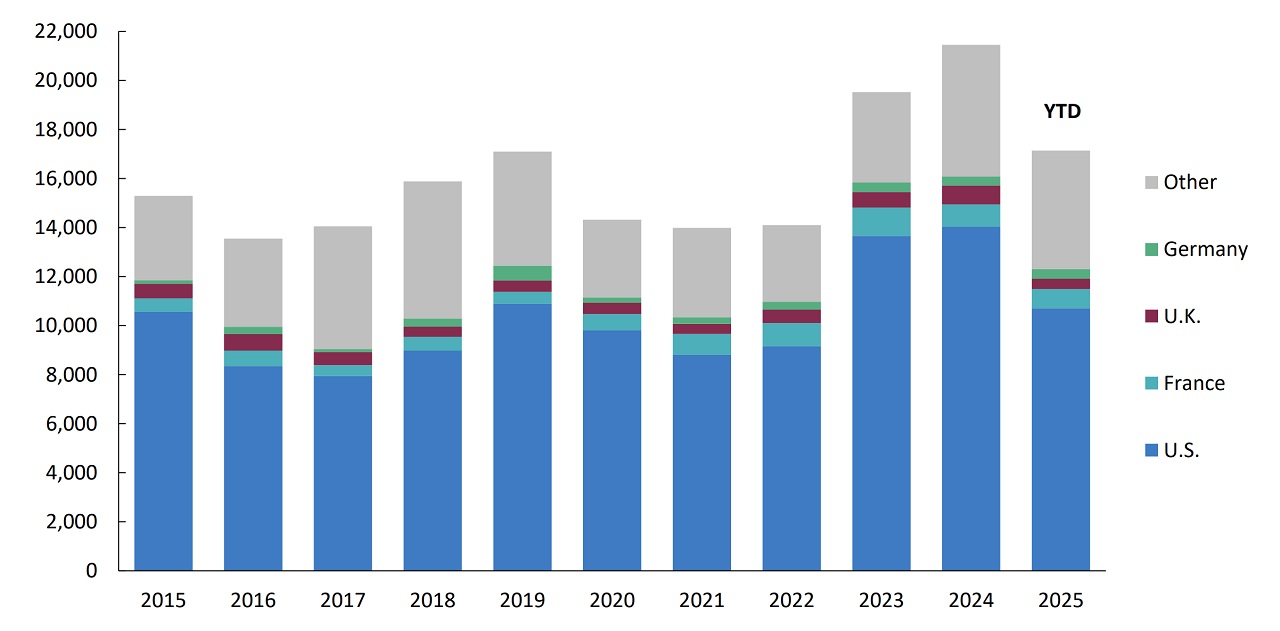

Figure 2: Canadian aerospace exports by top destinations (millions, nominal C$)

Source: Canadian International Merchandise Trade (CIMT) dataset

Note: YTD uses available data (up to October). Values are nominal, customs‑basis. Estimates are below AIAC equivalents, as the CIMT data definition is narrower.

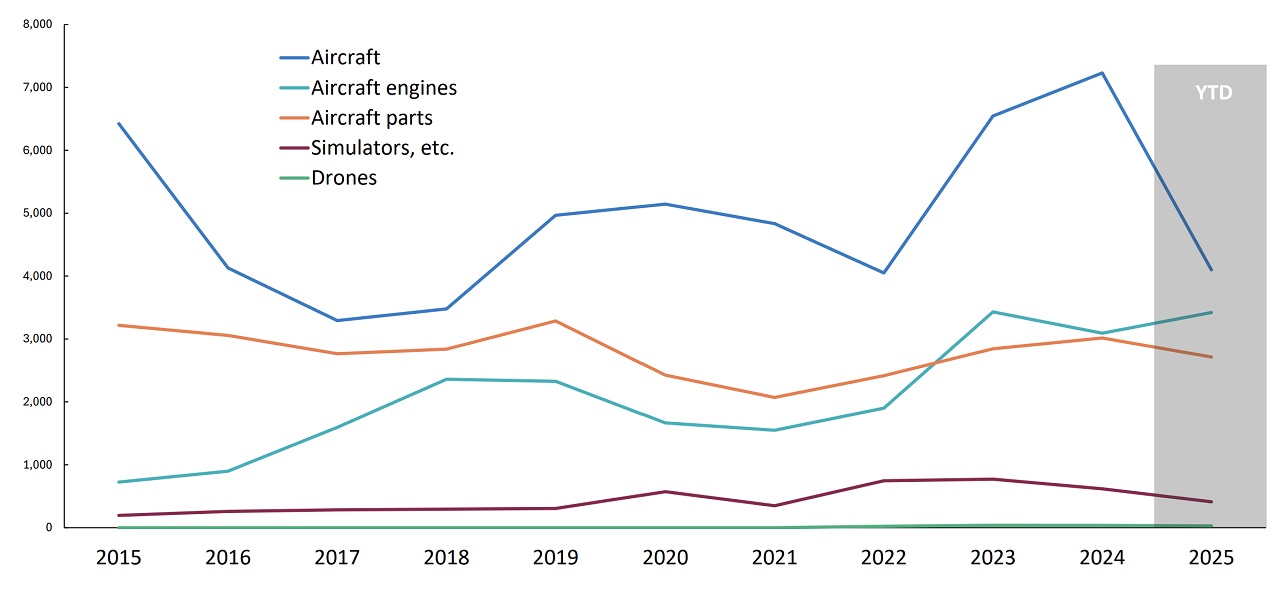

Figure 3: Canadian aerospace exports to the U.S. by product (millions, nominal C$)

Source: Canadian International Merchandise Trade (CIMT) dataset

Note: YTD uses available data (up to October). Values are nominal, customs‑basis. Simulator, etc. includes arrestors and launchers.

Export diversification opportunities for Canada’s aerospace industry

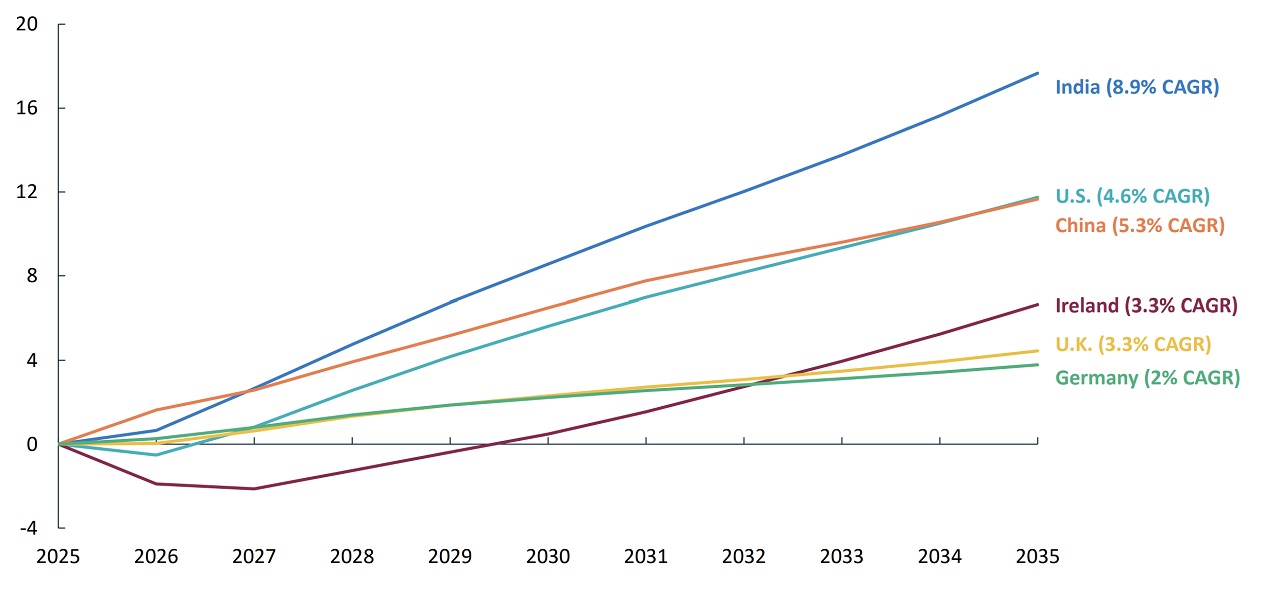

Figure 4: Countries with the largest projected aircraft import demand growth

Source: Oxford Economics Trade Prism

Note: Values are nominal imports of aircraft (e.g., HS 8802)