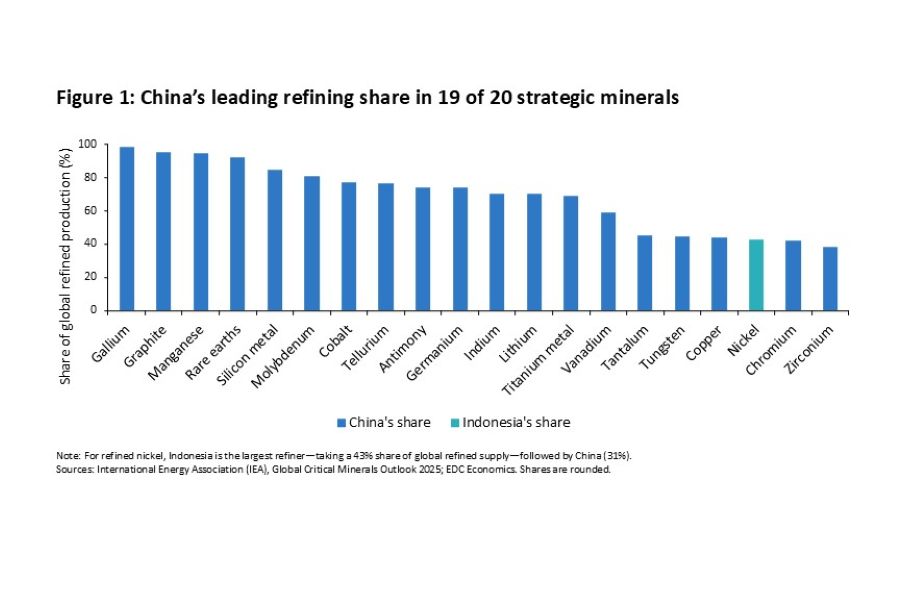

Taken together, these trends—security-driven demand, processing bottlenecks and rising metals demand linked to AI—frame both the opportunities and constraints shaping Canada’s critical minerals positioning.

Canada’s current export strengths remain concentrated in a small group of commodities, including aluminum, copper, potash, nickel and uranium, where large-scale production and supporting infrastructure are already established. By contrast, several policy priority minerals—such as lithium, cobalt, graphite and REEs—remain at an earlier stage from an export perspective.

A persistent challenge has been attracting risk-tolerant, long-term capital, particularly for capital intensive processing and refining. According to RBC, roughly 10% of mining capital raised in Canada over the past 25 years has flowed to critical minerals, reinforcing a long-standing “mine and ship” model where higher-value processing has largely taken place elsewhere.

More recently, investment momentum has begun to improve. Nearly half of all active mining proposals in Canada for 2024-2034 are now tied to critical minerals, representing more than $72 billion in potential investment. Recent federal measures focused on infrastructure, financing and processing are helping shift the focus from strategy to project execution.

Canada’s competitiveness is, therefore, increasingly execution-dependent. Access to low-emissions power and comparatively strong environmental and social standards are often cited as advantages as governments and end-users place greater emphasis on how critical minerals are produced. Converting these strengths into a stronger export position will depend on continued progress in permitting, infrastructure buildout (including power), integration into allied supply chains and the expansion of domestic processing and refining capacity.

Against this backdrop, Export Development Canada (EDC) supports Canada’s critical minerals sector by helping companies manage risk, access capital and integrate into allied supply chains as global demand and supply security pressures intensify.

New to EDC? Visit Export Help Hub to connect with a trade advisor and learn how we can support your export strategy. Already an EDC customer? Contact your relationship manager to discuss how current global developments may affect your business, or call 1-800-229-0575.