Simply put, Brazil still has considerable headroom. The country is expected to bring roughly 20 million hectares into production by 2031, one of the fastest area expansion rates globally and roughly equivalent to France’s total arable land area.

This expansion won’t be without challenges. Remote degraded pastures require significant investment in land conversion and rural logistics infrastructure. Climate change also presents risks, with research suggesting that changing conditions could weigh on projected land values and the financial viability of new conversion efforts.

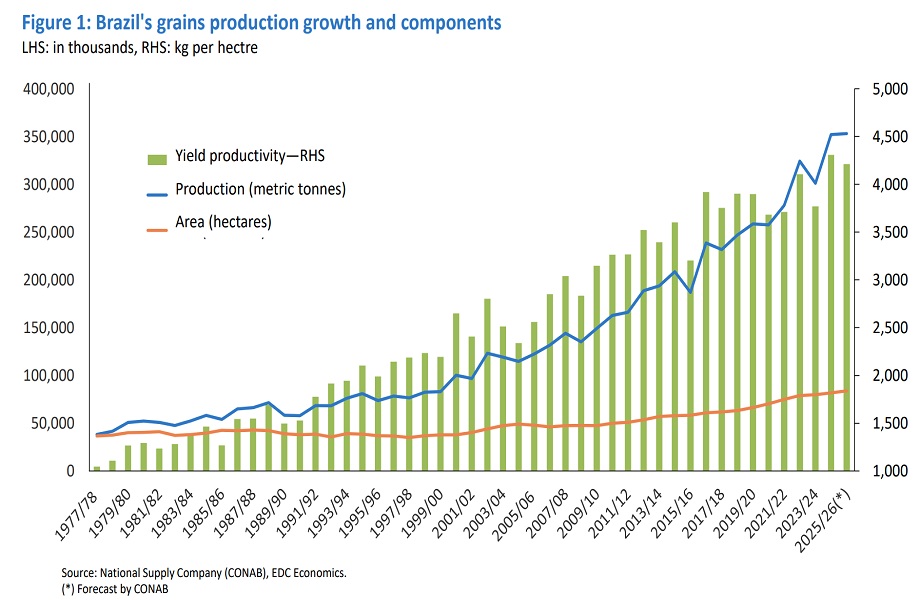

Yield growth will remain a key driver. While Brazil’s soybean yields are already world-class, yields for many other major field crops still lag those of global competitors. Yield gains will therefore remain a key structural driver of growth even as the rate of land expansion will eventually moderate. Fortunately, this maturation shift will not arrive any time soon. Official projections estimate Brazilian grain production will grow 27% through the 2033-2034 harvest compared to 2023-2024 levels, supported by both continued land expansion and further yield gains.

Near-term risks facing Brazil’s agriculture sector

Despite strong long-term fundamentals, near-term pressures are emerging. High interest rates, tighter credit conditions and elevated input costs have squeezed farm margins and contributed to rising bankruptcies.

Brazil’s heavy reliance on imported fertilizers remains a key vulnerability to geopolitical shocks, as ongoing conflicts have highlighted through price spikes and supply disruptions. Fiscal constraints also matter. Rising public debt could limit the government’s ability to expand funding for key support programs such as the Agricultural Plan (Plano Safra), Brazil’s main agricultural financing tool. Together, these factors could lead to short-term volatility in planting decisions and output, while stricter environmental compliance requirements continue to add regulatory and cost pressures. The foundations for long-term growth remain strong, but funding and structural constraints will shape the pace.

Why Brazil’s agriculture boom matters for Canada

Brazil’s growing influence in global agricultural markets has direct consequences for Canadian farmers and suppliers.

“Brazil’s farm boom opens the door to a wide range of opportunities for Canadian exporters,” says Ashley Kanary, EDC’s director of agri-food strategy. “Beyond wheat, pulses and specialty foods, demand is growing for fertilizers and soil health inputs, feed ingredients and additives, and ag-tech solutions tied to sustainability and yield gains—areas where Canadian expertise is highly competitive.”

From a market perspective, Justin Shepherd, senior economist at Farm Credit Canada, notes that “Canadian farmers closely monitor Brazilian grain production. Brazil’s harvest and export activities typically peak just before North American planting season, influencing U.S. futures prices. Consequently, spring planting decisions in Canada and the U.S. are affected by Brazil’s agricultural outcomes.”

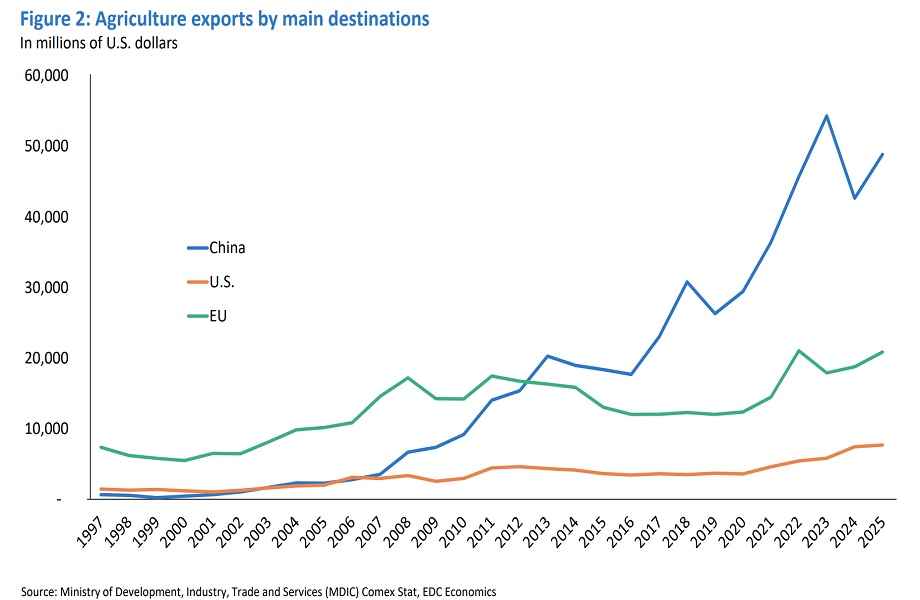

From a competitive standpoint, Brazil’s low-cost production intensifies pressure on Canadian exporters in Asia-Pacific and the Middle East, while the European Union-Mercosur Partnership Agreement and Interim Trade Agreement further improves Brazil’s access to European markets. Mercosur is the South American trade bloc that includes Argentina, Bolivia, Paraguay and Uruguay. Even so, Brazil’s agricultural expansion is creating new areas of strategic alignment with Canada.

Fernanda Custodio, EDC’s business development director for Brazil and the Southern Cone, says Brazil and Canada show strong complementarities in natural resources, particularly agribusiness, where both countries are leading global food producers.

“In Brazil, rising investment—largely driven by the private sector—is accelerating the country’s transition toward greater efficiency, productivity and competitiveness in agricultural goods and services. This shift is creating a strong pipeline of market-entry and expansion opportunities for Canadian companies, especially those offering advanced ag-tech solutions, digital tools and other high-value technologies that support the modernization of agricultural systems and supply chains,” Custodio says.

For Canadian firms, this alignment is translating into concrete areas of engagement. Brazil’s vast agriculture sector offers scope for Canadian agri-businesses, logistics firms, fertilizer suppliers and ag-tech companies—particularly in precision agriculture, sustainability solutions, digital crop monitoring, inputs and transport infrastructure.